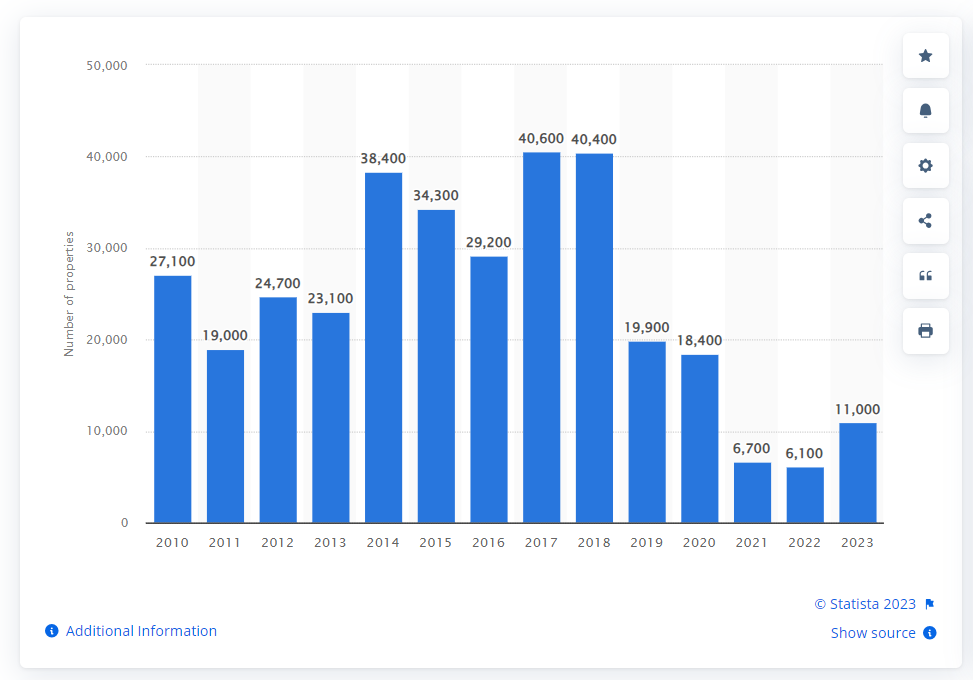

Chinese buyers comprise one of the largest groups of foreign buyers of residential property in the United States. In 2017, a record number of residential properties were bought by Chinese nationals, but since then, both the sales volume and percentage of all foreign-bought properties has declined. In 2023, Chinese buyers were responsible for 13 percent of all sales to foreigners.

Who is the biggest buyer of U.S. residential property?

During the coronavirus pandemic, buyers from Canadian and Mexican origin dominated international transactions, but in 2022 Chinese nationals bought the most U.S. residential property. They were also responsible for the largest share of the aggregate value of properties purchased. On average, Chinese bought properties were also substantially more expensive than the ones purchased by other buyer groups, such as Canadians.

How has the market developed?

The total property sales to foreign buyers peaked at 153 U.S. dollars in 2017, followed by a period of declining transaction value. The coronavirus pandemic has significantly contributed to cross-border transactions remaining subdued. In 2022, the value of property sales to foreigners was the lowest observed since recording began.

Published by Statista Research Department, Sep 27, 2023

Part One:

General Aspects of Purchase and Sale of Real Property

INTRODUCTION: REAL ESTATE TRANSACTIONS: IS A LAWYER REALLY NEEDED?

Ownership of land and improved property ("real property" or "real estate") within the United States has long been a goal and accomplishment of both citizens and noncitizens who arrive in this country. Both in terms of investment and in terms of acquiring a home, real estate transactions often form the single largest purchase of the average person and can be an excellent method to build up wealth. Recent tax laws have made the ownership of a home even more beneficial, not only allowing full deduction of interest on the home loan, but delaying or avoiding entirely capital gains upon the sale of a residence. When these tax benefits are combined with the steadily appreciating real estate market in California over the past five years, ownership of property has been seen to be the most intelligent major investment of the average American.

In the United States any legal entity (individual, partnership, corporation, or limited liability company, whether citizen of the United States or not) can own any real property and the laws of the state in which the property is located normally control the legalities of how to purchase, lease, sell, and use real property. Most understandings regarding real property are required to be in writing or are unenforceable, thus the written documents concerning property are of the highest import.

Increasingly over the past hundred years, the government has imposed additional obligations and controls over use of property, both in terms of allowed use ("zoning restrictions") and in imposing liabilities for various types of misuse (violations of building codes; violations of environmental laws such as improper disposal of waste materials on the property; etc.) Further, especially in the sale of homes, the government has imposed remarkably complex requirements of disclosure of problems and potential problems that the buyer may encounter, from defects in construction, to disclosure to the buyer of the property's location in flood or earthquake zones. The government has become a not so silent partner to every real estate transaction and the parties that ignore that fact take great risks.

It is an oddity that many people who would seek legal counsel for drafting a small will or suing someone who dents a fender on their car do not seek legal counsel when buying an asset which they may own for decades, which may cost a million dollars and which imposes thirty years of obligations on the buyer. Most people execute purchase documents or leases without bothering to carefully read the tens of pages of detailed legalese and only obtain legal advice when something goes wrong...and by then it is often too late. It is an obvious but often ignored fact that someone, sometime took the time and money to draft the complex form document that the real estate broker asks the buyer or seller to execute; clearly whoever drafted that complex document presented to the buyer or seller was drafting that long form for a reason, not at random. For a party to execute such a form without a full and complete understanding of its terms is equivalent to signing a blank check.

As with much of law, the best time to obtain legal advice is before a dispute or problem arises and it is a simple fact that a major portion of the contractual litigation in the United States involves real estate and alleged breach of leases or purchase agreements.

While real estate brokers and agents usually have form agreements, and while most landlords avail themselves of the preprinted form leases created decades ago by unknown persons, the fact of the matter is that these forms are usually antiquated, often inappropriate, and invariably a shock to the persons bound when they finally read them, usually long after signing them and after a heated argument with the other party. Properly drafted documents involving real estate are a necessity and more than any area of the law, written documents are usually required to form a binding obligation regarding real estate.

Another often ignored fact is that almost all professionals involved in real estate transactions have their own interests which do not necessarily conform to those of the buyer, seller, lessor or lessee. Real estate brokers and agents are usually only paid if a transaction culminates and are paid more if the transaction is higher in price. Clearly, such parties do not have an objective stance to take when examining the benefits and detriments of a particular transaction. Likewise, the lenders, the title companies, the builders, and the mortgage brokers are all interested parties who seek to have a transaction culminate simply because that is how they are paid.

If one seeks truly objective analysis of the cost benefit and detriments of a real estate transaction, and if one wishes an objective review of the contractual documents, one is compelled to seek expert legal advice from an attorney whose task is not to encourage the culmination of the transaction regardless of the consequences. It is the fact that attorneys so often advise of the negative aspects of transactions that have given them the reputation for being "deal killers." However, to consider both the good and the bad of the transaction is precisely why lawyers should be retained in real estate matters. One client put it well: often, the most money that can be made from a transaction is made by walking away from the transaction. Usually, the only professional who will so advise is the lawyer reviewing it.

TYPES OF REAL ESTATE TRANSACTIONS:

While the variations on the type of real estate transactions are as broad as the ingenuity of human kind, most transactions involve the purchase, sale, lease, construction, or subdivision of a piece of reality. The topics of commercial leases, rental of residences, construction and of subdivision of real property are each complex enough to justify a lengthy article in themselves and are the topics of other articles on this website. This article will, instead, concentrate on the general topic of purchase and sale of realproperty.

The Basic Purchase/Sale Transaction of Realty in California

The average purchase and sale of realty in California is comprised of the following parties and entities:

1. The Buyer;

2. The Seller,

3. Real estate broker or agent representing either the Buyer or Seller or, at times, both; sometimes two or more brokers are involved in the transaction.

4. A lending institution which finances the transaction;

5. A title company which examines the "chain of title" of the property to ensure that the Seller has title to sell to the Buyer and, in effect, acts as an insurance company insuring the validity of the title to Buyer;

6. The County Recorder who records the title documents showing ownership has vested in the Buyer (usually with a Grant Deed to the Buyer and Deed of Trust or Mortgage in favor of the Lender);

7. Often a mortgage broker who arranges financing between the Lender and Buyer;

8. Various experts who examine the condition of the property and create a report before close of the transactions (such as termite and dry rot inspectors; engineers, soil engineers, architects, etc.);

9. The escrow agent who holds the money and the title documents of all the parties and distributes them pursuant to written instructions;

10. If a condominium or home owners association is involved, that organization must be joined by the buyer.

STEPS IN THE TYPICAL TRANSACTION

While transactions may vary widely, the usual stages are:

1. A real estate broker shows a listed property to a prospective buyer. The buyer decides he/she wishes to make a bid and does so, usually rendering a few thousand dollar deposit along with the bid and signing a form that the broker usually supplies labeled, "Offer."

2. The broker presents the offer to the seller or the seller's broker and they can accept it (signing on the form), reject it, or counter offer with an offer of their own. The counter may involve a different price or different financing or requirements such as requiring buyer to pay for correction of defects discovered by the inspectors, etc. or perhaps accepting the Property "as is."

3. Each offer or counteroffer gives the other party the right to accept. If they accept before one withdraws an offer or counteroffer, both parties are bound. All offers and counteroffers must be in writing to be legally effective.

4. Once there is an acceptance, then within a time period listed in the documents the buyer normally is required to obtain financing, usually from a bank or savings and loan, while various inspectors such as termite and dry rot inspectors, soil engineers, etc, visit the property and render a written report as to its condition. The offer normally requires that the property "pass" all such inspections or the buyer may withdraw the offer and receive the deposit back. Quite often if the property fails to pass a particular inspection, the buyer and seller will negotiate as to who pays for the repairs...often they split them.

5. If financing is not possible, the deal falls through. If financing within the guidelines of the offer is achieved, then the buyer is bound and must proceed with the deal.

6. All deposits, inspection reports, title documents, down payment, bank documents and sums go to an escrow officer who holds the monies and documents pursuant to written instructions and only releases the various documents and sums to the parties when the conditions are met. The parties normally split the costs of the escrow officer. Buyer must also purchase enough insurance on the property to protect the lender if the property is destroyed or damaged and proof of insurance is also deposited into escrow.

7. One of the documents deposited into escrow is title insurance. This is a document prepared by a title insurance company that warrants that the title is in the name of the seller and that seller is empowered to transfer title to the buyer.

8. The brokers are normally paid from the sums deposited into escrow and the typical transaction has the Seller paid in full by a combination of the bank (who takes back a "deed of trust" or "mortgage") and the down payment of the buyer. Down payments are normally between twenty and thirty percent.

Thus, a typical transaction for a three hundred thousand dollar structure will have the following computations:

Down payment will be about sixty thousand dollars. The bank must lend $240,000. Closing costs (costs of escrow, title insurance and the like) will be about six or seven thousand dollars and the broker will be paid by the Seller between $15,000 to $20,000 for their fees. Buyers normally pay for the title insurance, half of escrow costs, and the inspections. Realistically, a buyer in the above scenario should plan on spending cash of close to seventy thousand dollars to close the deal while the Seller will only receive about $280,000 once the broker and the escrow people are paid.

THE ROLE OF THE REAL ESTATE BROKER

In the United States the overwhelming majority of transactions involve real estatebrokers who are licensed professionals who receive, usually, a percentage of the sales price of the property being sold (the "commission.") A broker has a fiduciary duty (duty of loyalty) to the person represented and can only represent both the buyer and seller if they both consent. Usually two brokers are involved and they split the commission which is normally between five and six percent of the selling price of most property. The commission is paid from escrow upon the close of the transaction. The commission is NOT set by law and may be negotiated with the broker.

Brokers take on the bulk of the work of the real estate transaction, seeking property to show to a prospective buyer or showing the listed property of sellers. Brokers often have access to computerized listings of all property for sale thus can quickly ascertain what property may be appropriate for a buyer.

Brokers normally have written contracts with their clients and those contracts, like their commissions, can be negotiated but often are not since most laypersons are intimidated by the lengthy form contracts presented to them by the broker. Most such contracts give the broker an "exclusive" right to list the property for a stated period of time, such as ninety days, during which only the broker can sell the property.

As experts, brokers can often give valuable advice as to the negotiations occurring, the proper price to bid, and the dangers involved in the location of the property, etc. Brokers normally have complex long legal documents which they suggest their clients execute to both bid, accept bids, counteroffer and culminate the sales transaction. These forms, written by the brokers' associations, are quite complete and fully binding on the parties. Just reading such documents can take well over an hour and most buyers or sellers, in a hurry to place or accept a bid or counteroffer, do not bother to carefully read the terms.

Indeed, most brokers simply use the forms without careful analysis of their contents, having received the forms from their associations and usually using them for years without a second thought.

A broker earns nothing if a sale does not occur. This necessarily creates a bias in the minds of most brokers in that they seek to encourage culmination of any sales transaction. Further, the higher the price, the more they earn. While this may seem fine for the seller and bad for the buyer, it actually also distorts their advice even to a seller since they will often recommend costly improvements to the property to help it sell which, of course, increases the sales price thus the commission.

Most brokers are honest and hardworking. It is a competitive and stress filled job requiring long hours on weekends and nights. Nevertheless, while their role is extremely valuable, a wise seller or buyer understands that their economic position within the transaction makes objective advice hard to obtain from a broker.

THE LENDER

Either by use of a mortgage broker who seeks possible loans from banks, or via the broker who usually has connections with various banks, or on their own, the average buyer does not buy real estate for cash but purchases it by borrowing most of the sales price from a bank or savings and loan association. The usual transaction requires a twenty to thirty percent down payment, with fifteen to thirty year financing for the remainder of the purchase price. Thus a three hundred thousand dollar home will normally require a down payment of anywhere from sixty to ninety thousand dollars plus a loan for the remainder, at interest rates that vary but will normally be around seven to ten percent over thirty years. Bank loans come in an enormous variety of terms including variable interest rates, graduated payment schedules, federally insured, etc, etc.

Several thousand dollars are also spent to arrange the loan ("points") and to arrange for title insurance on the title, perform the termite and dry rot inspection to determine the condition of the property, and to obtain the insurance that any lending institution will require before loaning on the property. It is typical to spend perhaps five thousand dollars to "pay" for the loan before the first payment is due.

Most loans in California are secured with a document called a Deed of Trust on the property being financed. Without going into detail, the Deed of Trust allows the lender to foreclose and seize the property by an out of court procedure should payment not be made in a timely manner. Normally, the procedure for foreclosure is to record a Notice ofDefault in the recorder's office which gives the borrower ninety days to cure the default by paying all sums due and the costs of the foreclosure recordation. At the end of ninety days, if no payment has been made, the Notice of Sale is recorded and the right to cure the default in payment expires. The lender can then sell the property to pay down on the loan.

In California, there is no deficiency judgement; that is, assuming the property is a home which the buyer can no longer afford, if the lender forecloses on the property the lender can not also sue the borrower for the difference between the proceeds of the foreclosure sale and the amount due under the loan. Nevertheless, the borrower who suffers such a foreclosure normally has his or her credit history ruined for many years.

CONCLUSION:

The tax benefits of ownership of realty and the usual appreciation of property in California are added incentives for the ownership of property but it must be recalled that real property in California, over the past hundred years, has averaged perhaps 8% appreciation a year and if appreciation for a period exceeds that, it must be expected that there will be years of depreciation to counterbalance the previous rise. In the last twenty years real property has decreased in price for periods of three to five years three or four times and it is critical for the buyer to recall that a vibrant and expanding economy must ultimately end, at least for a period. One must not automatically purchase property relying on future appreciation to justify the debt incurred since location, the surrounding economy, and just plain luck can often have drastic effects on value of property.

Nevertheless, careful and planned purchase of real property has been the typical method of appreciation of wealth for new citizens and Americans alike and an expanding population seems to assure that while cycles may cause temporary downturns in the market, that overall the demand for realty will continue to expand.

(Quelle:https://www.stimmel-law.com/)

与许多国家规定只有本国公民才可以拥有土地不同的是,美国法律对外国人购买、继承、拥有土地的规定与本国公民没有什么不同,一视同仁;外国人可以购买土地、继承土地所有权,也可以购买房产,由于房产与土地是连在一起的,购买房屋时,往往同时拥有了房屋所在土地的永久所有权。

外国人在美国购买房地产虽然没有什么法律限制,但值得一提的是,有些居住小区、高层公寓、合作公寓以及老年社区的管理委员会对房产购买有特别的审核规定,目的是保证本小区居民的素质,因此外国人购买者在投资这些房产时事先应了解清楚相关规定。

美国土地

在美国的房地产市场,外国买家一直很活跃,据全国房地产经纪人协会(National Association of Realtors)的统计,在2016年4月到2017年3月的12个月中,外国买家购买的房地产价值1530亿美元,比上一年同期增加49%,创历史新高。这个数字大出经济学家的预料,因为这一时期美元走强,相对来说美国的房地产就显得比较贵,但外国买家显然并没有被美元走强吓到,还是大举投资美国的房地产,外国买家总共购买了28万栋房产,这个数目比上一年同期增长了32%。

从总体上看,外国买家占现房买卖额的10%以及现房买卖数量的5%,这说明外国买家购买的房地产平均价格是美国人的一倍。在所有外国人购买的房地产中,以卖买额来看的话,一半集中在佛罗里达、加利福尼亚和德克萨斯三个州。此外,新泽西、亚利桑那、纽约、华盛顿特区也是外国买家青睐的州。

现在到美国置业买房的人越来越多,我们今天就来谈谈在美国购买了房地产,是否拥有土地的所有权,如果有的话,是否有年限或其他限制。

美国的国土面积982万平方公里,除掉66万平方公里的水面,土地面积为916万平方公里,其中大约三分之一强归政府所有,其余为私人财产。

在美国购买的房地产,通常说的都是土地和地上建筑等不动产,业主对它们拥有永久产权,可以作为遗产由后代继承,也可以捐赠或出售。在许多地方,业主每年要向地方政府交纳房地产税,用做当地中小学教育和其他方面的经费。房地产的价值会随着市场波动,业主如果将房屋出租的话,在报税时可以用建筑物的折旧冲抵收入,但是历史趋势来看,美国房地产会持续升值。

土地作为房地产的一部分,业主拥有它的产权,地表和地下的自然资源除非有法律规定,通常也都是业主的财产。

单门独户房产的情况比较简单,业主直接拥有房屋与土地的产权。自从1960年代以来,联邦、州以及地方政府出于环境保护等方面的考虑,对于私人土地上的野生动植物和其他环保事项可能制定有相关的法律法规,业主需要了解并遵守。

以西雅图市为例,如果业主的地块位于环境保护的敏感地区,例如陡坡、野生动物栖息地和湿地等,在未经许可的情况下,不得砍伐任何林木或者破坏地表植被。在其它尚未开发的土地上,未经专业人员鉴定具有危险,不得砍伐直径6英寸(7.5厘米)以上的树木。如果地块已经开发,除非经过鉴定有危险,不得砍伐任何具有历史、生态或美学价值的树木,其他直径6英寸以上的树木一年内砍伐不得超过3棵。尚未利用的土地业主打算开发,则在申报批准建房的地段管制相对宽松,但是也必须符合该市的绿色评估标准,尽可能对环境加以保护和美化。

一般来说,如果房产位于统一规划开发的社区,而且居民组织有小区业主管理委员会,则大家共同拥有对涉及公共领域事务的管理权,表现为具有法律效力的小区建筑规范与章程。例如有的居民小区对房屋的外观式样和颜色有严格的规定,不得随意增添附加建筑,甚至连邮箱的颜色规格和门牌号码等都需要符合标准。

至于公寓房屋,一般的公寓业主与单门独户一样拥有自己单元的房屋产权,至于公共区域例如大楼前厅、走廊和电梯楼梯间、非付款购置的公共停车位以及健身房休闲设施等,包括公寓楼的地皮,则属于所有住户共有。美国还有很多地方有合作公寓,它们表现为所有业主组成的非营利公司,每个业主购买的是相应于自己单元的该公司股份,所以其土地权利也是表现为股份形式,其它方面与公寓没有实质的区别。

美国私有土地的地下资源,通常也是属于业主所有,但是其权利可能与地上建筑分开,所以在那些矿藏丰富的地区购买地产时,要特别注意是否包括地下资源的权利。在这方面,几乎所有的州都有相应的法律加以规范。

地表与地下资源捆绑在一起的地产,在美国被称为“单纯费率房地产”(fee simple estate)。100多年前在俄克拉何马、得克萨斯以及美国南部海湾地区发现大量石油,企图发财的人们纷纷涌入投资“黑金”,连带使得地产交易复杂化,人们开始将地表和地下资源分别出售。我们的下一篇博文将介绍这方面的情况。

(Quelle:https://share.america.gov/)